Most people don’t realize debt collectors often accept 30% to 50% of the actual amount owed.

Smart negotiations with creditors can cut your debt by 20-50%, easing the burden of overwhelming financial obligations. The process needs careful planning though. People often ask about negotiating with creditors and settling debts without hurting their financial future.

You can definitely negotiate with creditors. Learning to negotiate debt can help your financial recovery a lot. Debt settlement usually takes 2-4 years. You need a clear picture of your monthly payment capacity before starting.

This piece shows you how to reduce debt through creditor negotiations step by step. We cover your credit report details that show your payment history and shape your negotiation power. You’ll also learn your rights under the Fair Debt Collection Practices Act. Your journey toward financial freedom starts here!

Understand the Debt Before You Negotiate

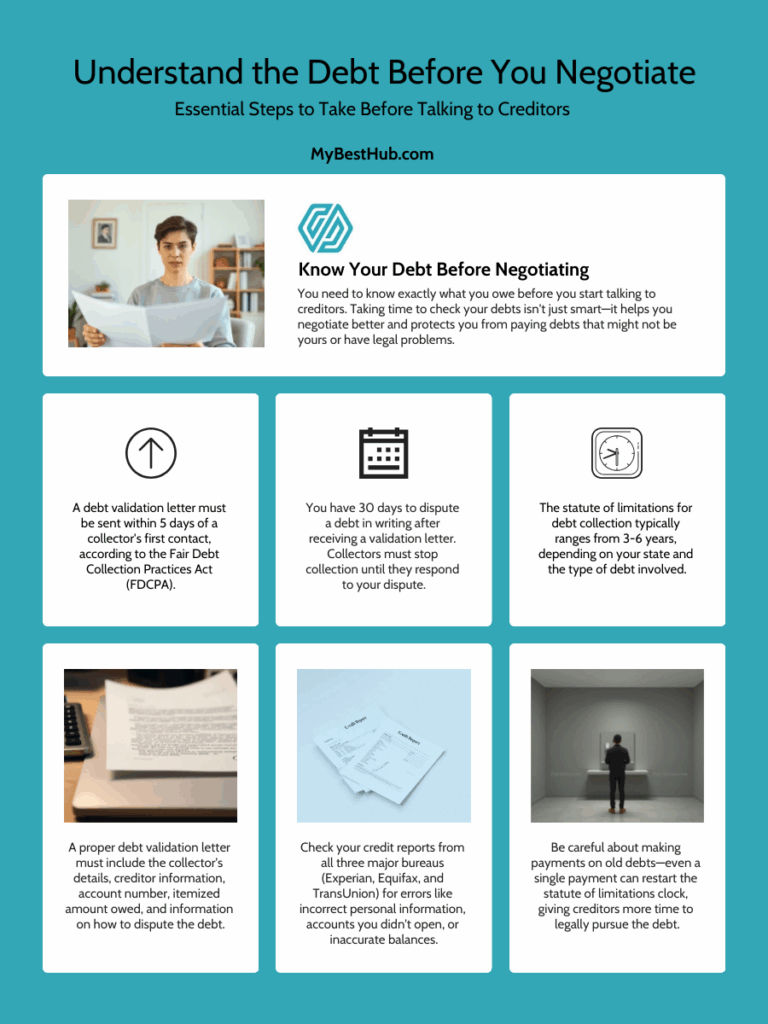

You need to know exactly what you owe before you start talking to creditors. Taking time to check your debts isn’t just smart—it helps you negotiate better and protects you from paying debts that might not be yours or have legal problems.

Request a debt validation letter

Your first move should be to get a debt validation letter. This document tells you everything about your debt and shows if the collector can legally collect from you.

The law says debt collectors must send you a validation notice within five days after they first contact you. They break the Fair Debt Collection Practices Act (FDCPA) if they don’t do this. This rule protects you from fake collection attempts.

A proper debt validation letter must include:

- A statement that the communication is from a debt collector

- Your name and mailing information, along with the collector’s details

- The name of the creditor you owe the debt to

- The account number associated with the debt

- An itemization of the current amount owed (including interest and fees)

- Information on how to dispute the debt

Ask for this letter right away if you haven’t gotten one. Read it carefully once you get it. You have 30 days to dispute the debt in writing. The collector must stop trying to collect until they properly answer your dispute.

Check your credit report for accuracy

Your credit report plays a big part in how well you can negotiate with creditors. Making sure it’s correct should happen before any talks begin.

AnnualCreditReport.com lets you get free copies of your credit reports from all three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. The three bureaus now let you check your credit report weekly at no cost.

Look for these things in your report:

- Incorrect personal information

- Accounts you didn’t open

- Inaccurate balances or credit limits

- Payment history errors

- Outdated negative information

Tell both the credit bureau and the business about any mistakes you find quickly. The credit bureau has 30 days to look into your dispute. Fixing these issues makes your position stronger when you try to reduce your debt.

Know the statute of limitations in your state

The statute of limitations on debt could change how you handle creditor talks. Each state sets a legal time limit for creditors to sue you for collecting a debt. This usually runs 3-6 years, based on where you live and what kind of debt you have.

The debt becomes “time-barred” after this period ends. Creditors can’t get a court order to make you pay. They can still try to collect and contact you about it.

The countdown starts from your last payment date. Be careful though—just one payment or writing that you owe the debt can restart the whole timeline.

This creates an interesting choice: waiting might work better than negotiating if a debt is almost time-barred. Sometimes letting the debt reach its limit gives you more power in settlement talks.

Check if your debt’s statute of limitations is ending soon in your state before you start any negotiations. This info can change your whole approach and might save you money.

Decide If Negotiation Is the Right Move

Debt settlement companies might tell you to negotiate with creditors, but this isn’t always your best move. You need to check your debt details and assess if settlement makes sense for your situation.

When to think about settling debt

You might want to talk to your creditors if:

- Your debts are way overdue and close to charge-off status (90-180 days past due)

- You have cash ready for a lump sum payment

- Bankruptcy looks like your only other option

- You can’t pay off unsecured debt within five years, even with deep budget cuts

- Your unpaid unsecured debt is half or more of what you earn

Most people can resolve their debts through settlement in 2-4 years. This works faster than other options. Once you reach an agreement, collection calls stop and your debt stays out of collections.

Risks of restarting the statute of limitations

You should be very careful about actions that restart the statute of limitations clock. Many states will reset the legal timeframe if you:

Pay even a small amount on old debt – this resets the clock for everything you owe. Writing down that you owe the debt can also restart the statute of limitations. Even casual talks about owing money might accidentally give creditors more legal rights.

This creates a tough situation. Trying to work things out with creditors could give them more time to sue you. If your debt’s statute of limitations is almost up, waiting might give you better bargaining power than rushing to negotiate.

Other ways to handle debt

Before jumping into creditor negotiations, look at these options:

Nonprofit credit counseling services provide debt management plans. These plans cut your interest rates and combine payments without hurting your credit like settlement would.

Debt consolidation loans put all your debts into one loan with lower interest. You’ll pay everything back instead of settling.

Bankruptcy gives you legal protection and a clean slate by clearing or reorganizing your debts. Your credit report will show bankruptcy for 7-10 years, but this could work better than settlement in some cases.

You can also try talking to creditors yourself instead of hiring a company. Many creditors will work directly with borrowers. This saves you from paying big fees to settlement companies (which run from $500-$3,000 or more).

Note that debt settlement usually hurts your credit score. You might owe taxes on forgiven debt, and creditors don’t have to negotiate with you. Still, if you’re in a tough financial spot, working with creditors might be your most practical choice.

How to Negotiate Debt with Creditors Step-by-Step

You’ve decided negotiation is your best option. Now it’s time to prepare your strategy to negociate with creditors. A good strategy can save thousands of dollars and help you get back on your feet financially.

Figure out what you can afford

Successful debt negotiation starts with knowing what you can actually pay. You need to create a detailed budget before reaching out to any creditor. Take a close look at your income and essential expenses like rent, utilities, and food. This will help you calculate the money available for debt repayment.

This step deserves your full attention. Get into your bank statements and find any non-essential expenses you could cut temporarily. Your careful analysis will give you solid facts for negotiation and shows you’re serious about fixing the debt situation.

Simple spreadsheets or online calculators can organize your finances better. Creditors will likely accept your offer if they see it’s the most you can possibly pay.

Make a lump-sum or partial payment offer

These approaches work well when you’re ready to negociate with creditors:

- Lump-sum settlements: Offer a one-time payment below the full amount owed

- Partial payment plans: Suggest smaller regular payments over time

- Interest rate reductions: Request lower interest or waived fees

Start by offering 50% or less of your debt for lump-sum settlements. Cash gives you power in negotiations. Creditors usually prefer getting money now instead of waiting for payment plans. Make your offer in exact dollar amounts rather than percentages to keep things clear.

Be honest about your financial situation

Open communication is the life-blood of good negotiations. Tell creditors clearly about your situation when you negociate with creditors—whether it’s losing your job, medical bills, or other hardships. Your honesty helps them understand why you can only pay the amount you’re offering.

Stick to facts instead of emotions. Keep records of every conversation, including who you talked to, when, and what was discussed. Good records protect you and keep negotiations consistent.

Avoid agreeing to more than you can pay

Debt collectors often use pressure tactics to push for quick payments. They might say you need to act now to avoid legal trouble. Don’t give in—never promise payments that bust your budget.

Agreeing to payments you can’t afford could lead to another default and possible legal issues. Stand firm on what you can pay. Most importantly, get everything in writing before sending money.

Your agreement should clearly state that your payment completely settles the debt. Look for words saying the account is “settled,” “paid in full,” or “accepted as settlement in full”.

Protect Yourself During the Process

Your protection from potential abuses matters just as much as getting a good settlement when you negociate with creditors. Strict regulations in the debt collection industry protect consumers throughout negotiations.

Know your rights under the FDCPA

The Fair Debt Collection Practices Act (FDCPA) sets clear limits on what debt collectors can do. You have the legal right to fair treatment whatever you owe. Debt collectors need your permission to contact you before 8 a.m. or after 9 p.m. They must stop calling your workplace once you tell them such calls aren’t allowed.

Debt collectors must give you “validation information” about what you owe during their first call or send it in writing within five days. They need to pause all collection activities if you ask for verification within 30 days, at least until they’ve properly responded.

Watch for illegal collection tactics

Spotting illegal collection behaviors helps you stay in control when you negociate with creditors. These practices aren’t allowed:

- Threats of arrest, violence, or empty legal action

- Excessive calls (more than seven times within seven days)

- Using obscene language or abusive communication

- Collecting unauthorized fees not in your original contract

- Public social media messages about your debt

- False statements about the debt amount or collector’s identity

The Consumer Financial Protection Bureau or your state attorney general can help if collectors break these rules.

Keep detailed notes of all communication

Good records are a vital protection as you negociate with creditors. Make sure you:

- Write down each call’s date, time, and representative’s name

- Document all claims about your debt and settlement offers

- Keep copies of emails and letters

- Get written confirmation before paying anything

These records become valuable evidence if any issues come up later. Send important messages through certified mail with return receipt to prove delivery. Recording calls might help too, if it’s legal in your state – just remember to tell the other person you’re recording.

Finalize the Agreement and Follow Through

A written agreement protects your finances after you reach a deal as you negociate with creditors. Getting everything in writing helps avoid future disputes and safeguards your interests.

Get the settlement terms in writing

You should never send money until you have a written settlement agreement. This document needs to clearly show that your payment will be accepted as “payment in full” for the debt. Your written agreement must include your account number, the settlement amount, payment deadlines, and a clear statement that the creditor won’t ask for more money. A good settlement letter typically reads: “We have agreed to accept your payment of $[amount] for [account number] by [date], as payment in full for this account”.

Use traceable payment methods

Secure, traceable payment methods are your best option. Certified checks or cashier’s checks give you better protection than personal checks. On top of that, it makes sense to send payments through certified mail with return receipt requested to prove delivery. You should never share bank account details or let creditors withdraw money from your accounts automatically.

Save all documents for future reference

Keep your settlement paperwork forever. These records are a vital shield if the creditor reports wrong information to credit bureaus or tries to collect the debt again. Yes, it is smart to ask for written confirmation once you’ve paid your debt fully.

Conclusion

Successful negotiation with creditors needs preparation, knowledge, and persistence. A clear understanding of your financial situation before talking to creditors gives you better control during discussions. You can approach negotiations confidently when you have proper documentation and know your rights.

You must verify your debts, understand the statute of limitations, and assess what you can realistically pay. The most vital part is honesty – with yourself about affordable payments and with creditors about your financial status.

Your rights under the Fair Debt Collection Practices Act protect you from unfair treatment while negotiating with creditors. This protection helps prevent potential abuse from collectors who might try illegal tactics.

Debt settlement takes time. Your original agreements turn into financial freedom through patience and consistent follow-through. Always get settlement terms in writing before you send any payment.

Your decision to negotiate with creditors should line up with your overall financial goals. Debt settlement might affect your credit score for a while. This approach often brings faster relief than multi-year repayment plans. These strategies can help you regain control of your finances and build a more secure future, whether you negotiate yourself or seek professional help.

Key Takeaways

Successfully negotiating with creditors can reduce your debt by 20-50%, but requires strategic preparation and knowledge of your rights to achieve meaningful financial relief.

• Always verify debt accuracy and request validation letters before negotiating—you have 30 days to dispute debts legally

• Start lump-sum settlement offers at 50% or less of what you owe, but only commit to amounts you can realistically afford

• Know your state’s statute of limitations on debt—making payments can restart the legal collection timeframe

• Document all communications and get settlement agreements in writing before sending any money to protect yourself

• Use the Fair Debt Collection Practices Act to stop illegal harassment and ensure fair treatment throughout negotiations

The key to successful debt negotiation lies in thorough preparation and understanding your legal protections. By verifying debts, knowing what you can afford, and documenting everything, you create a strong foundation for reducing your financial burden while avoiding common pitfalls that could worsen your situation.

FAQs

When negotiating effectively, you may be able to reduce your debt by 20-50%. Some debt collectors are willing to accept as little as 30% to 50% of what you actually owe.

Before negotiating, request a debt validation letter, check your credit report for accuracy, and understand the statute of limitations on your debt in your state. This preparation will strengthen your position during negotiations.

Yes, there are risks. Negotiating can potentially restart the statute of limitations on your debt, allowing creditors more time to sue for payment. It may also impact your credit score and result in tax liability for forgiven debt.

Know your rights under the Fair Debt Collection Practices Act (FDCPA), watch for illegal collection tactics, and keep detailed notes of all communications. Always get settlement terms in writing before making any payments.

Use secure, traceable payment methods such as certified checks or cashier’s checks. Send payments via certified mail with return receipt requested to prove delivery. Avoid providing bank account information or agreeing to automatic withdrawals.